Survival Analysis

The cancellation of accounts provides a direct application of survival analysis. This kind of analysis is usually used to estimate customer lifetime values. In this framework, customers are considered to have "died" when they cancel their policy, and the patterns in claims indicate whether the customer is alive. For example, a customer who regularly makes a claim every 2-3 months for years is probably still around if their last purchase was a month ago. A customer who set up their policy, make a bunch of claims, then went quiet for a year-less likely "alive". We use the lifelines and lifetimes python packages to assist in this analysis.

We will utilize 3 traditional features for this analysis:

- Frequency-The total number of claims - 1

- Recency-The time difference between the first and last claim

- T-Equivalent to the lifespan variable, total age of the account, or time between the cancel date and enroll date if canceled.

Survival analysis gives us an opportunity to predict future claims.

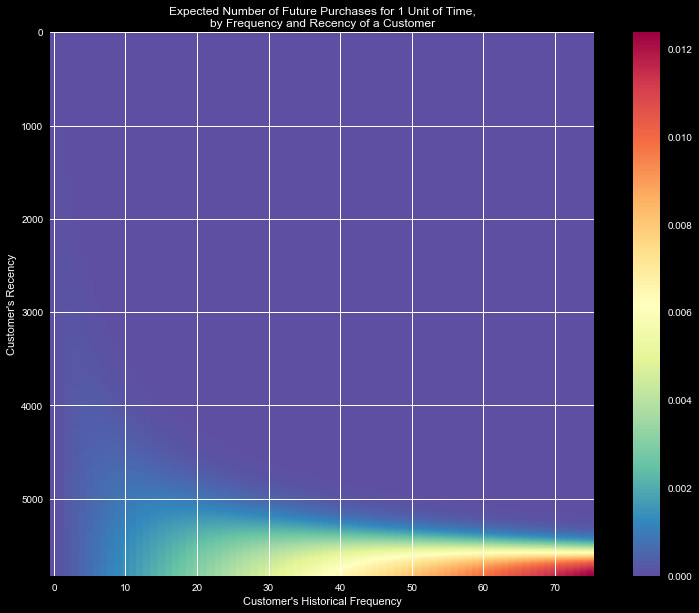

Figure 1 shows the expected number of purchases/day, as a function

of frequency and recency. Broadly speaking, only high recency

(indicating purchasing over large time frames) leads to a likely

to continue to make claims. A high frequency further increases this

likelihood, however recency is the dominating factor.

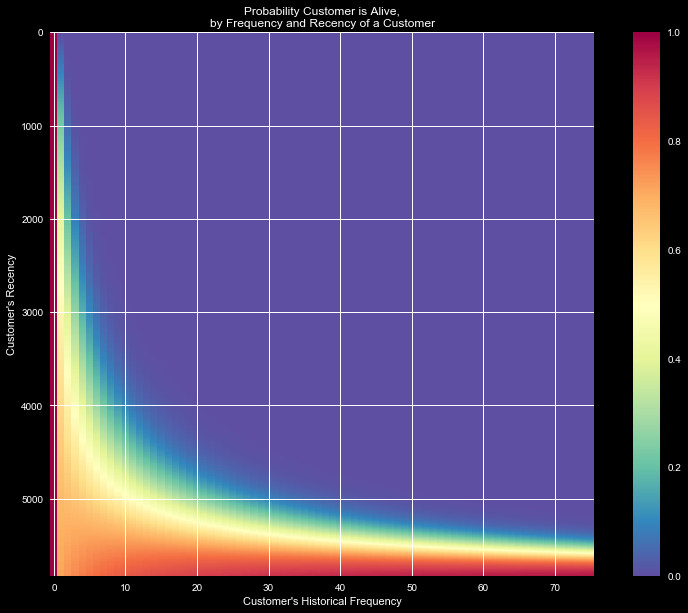

Figure 2 shows the likelihood that a customer is "alive" given purchasing

habits. Clearly high frequency and recency indicate an active and happy

customer that will keep returning, but we see that even a low

frequency customer with low recency stands a good likelihood of being alive.

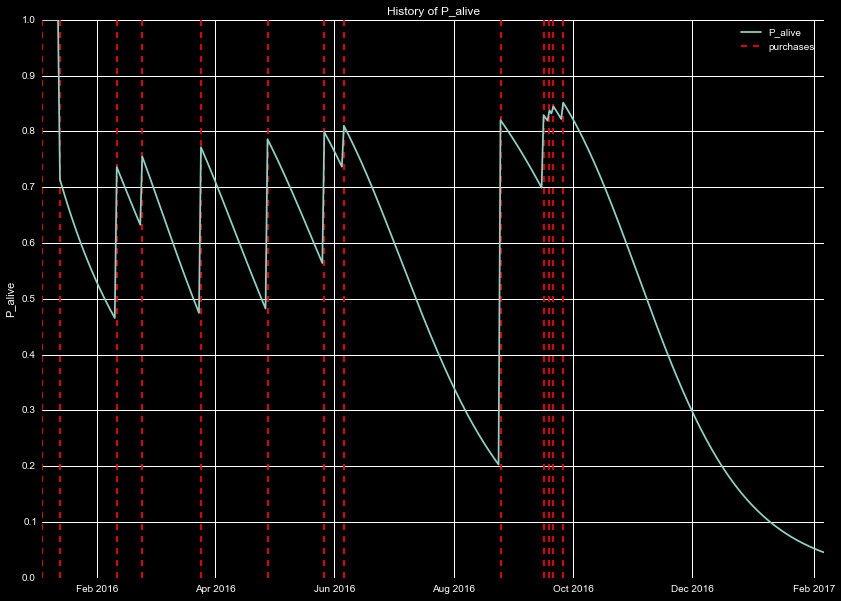

To see how this behavior changes over time, we can watch the likelihood

of being alive for a few individual cases. In Figure 3, we watch the creation

and "death" of a policy. We see when the account is created, the policy

is definitely alive (P=1), and shortly claims are filed. Each time a claim

is filed the likelihood of being alive jumps higher, however the likelihood

of the policy remaining alive decays. After June 2016 the frequent purchases

stop, and the account seems to have died. This is followed by a spike

in purchases, increasing the recency and frequency-until the last claim,

when the account looses activity, and the policyholder becomes very likely to leave.

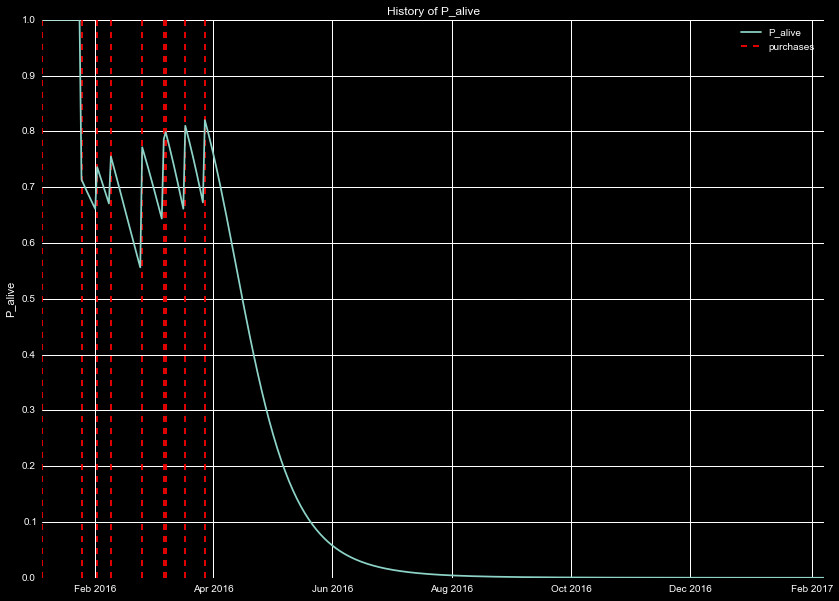

Figure 4 is the same as Figure 3, but for a different policy. This one is

in stark contrast to the behavior in 3, where the policyholder

Next, we look at the survival function of the entire population, S(t). The

survival function is a measure of the the number of policies that "survive"

until time t. This is important due to data censoring, or the effect where

we will see some cancellations, and not others, due to the time limited

nature of our data. Any policies that have not canceled by the end of our

time set (that we are predicting the cancellations for), are considered

right-censored. The survival function is calculated at each time by examining

the number of policies that were alive at time t, and the number that

canceled at time t. This is a way to include the censored data, and include

it into our analysis, despite the fact we do not see their cancellations.

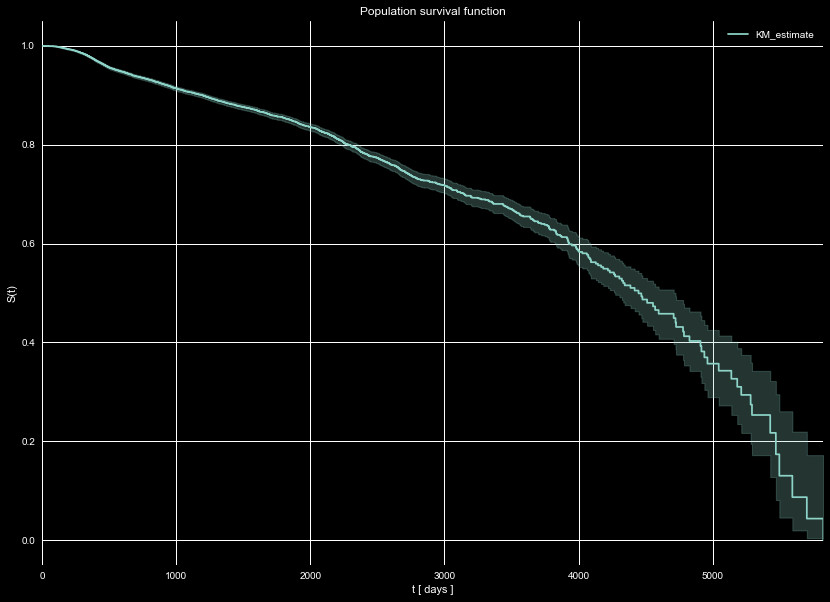

We show the survival function of our entire population in Figure 5, using

the Kaplan–Meier estimator. We see that half of the policies are expected to

survive to the 12 year mark (~4500 days) from the provided data. Note it is entirely

possible that this does not reflect normal behavior, depending on how the data

set provided was selected. We already saw cancellations were limited to 2016,

so there may be unknown, hidden biases in the data. That notwithstanding,

this is the expectations we have for our population to survive past a given time.

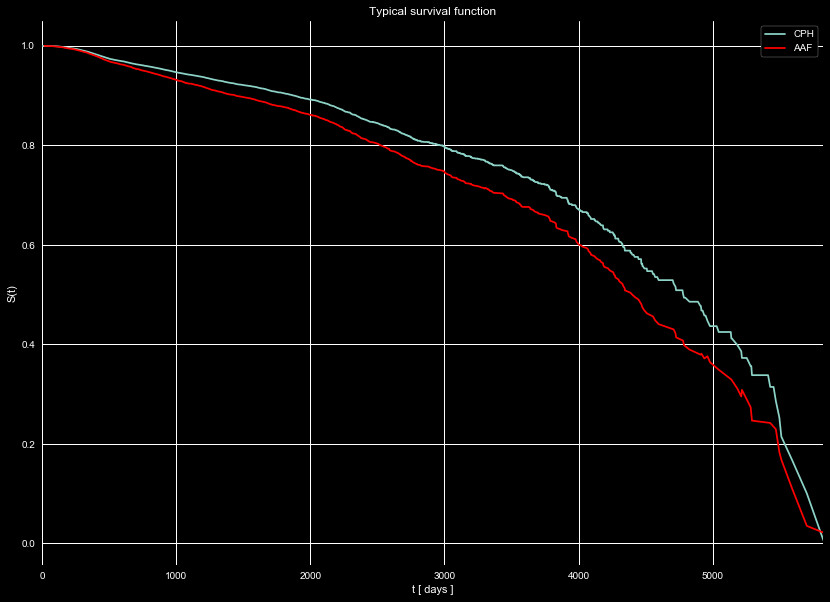

Survival functions are powerful tools, they can be used to estimate policy

lifetimes and customer lifetime values. Some estimators even allow for

the creation of individual survival curves based on the input features. In

Figure 6 we show an individual survival function for a typical policy

(recency of 130 days, frequency of 3), using two different estimators.

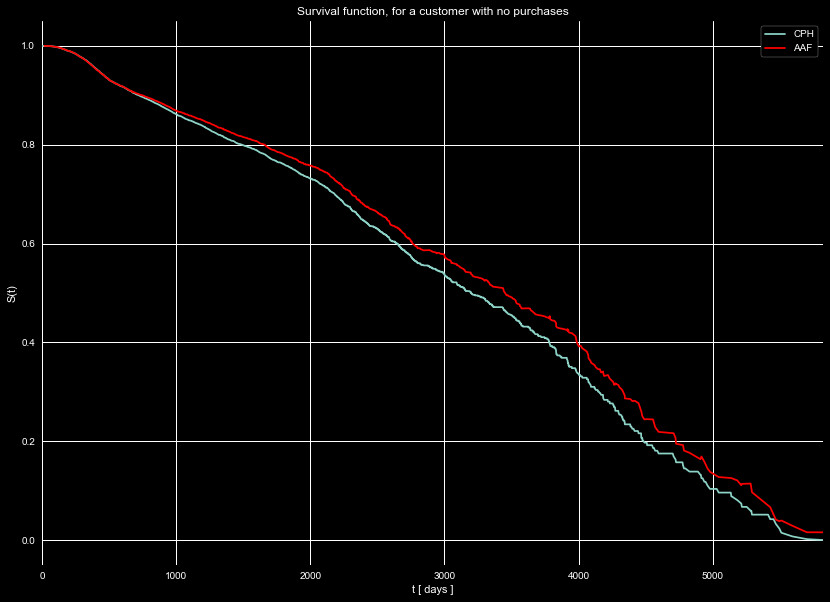

Figure 7 shows the same estimators, but for a policy with no purchases.

Note how policies with purchases tend to last longer than policies without

purchases.

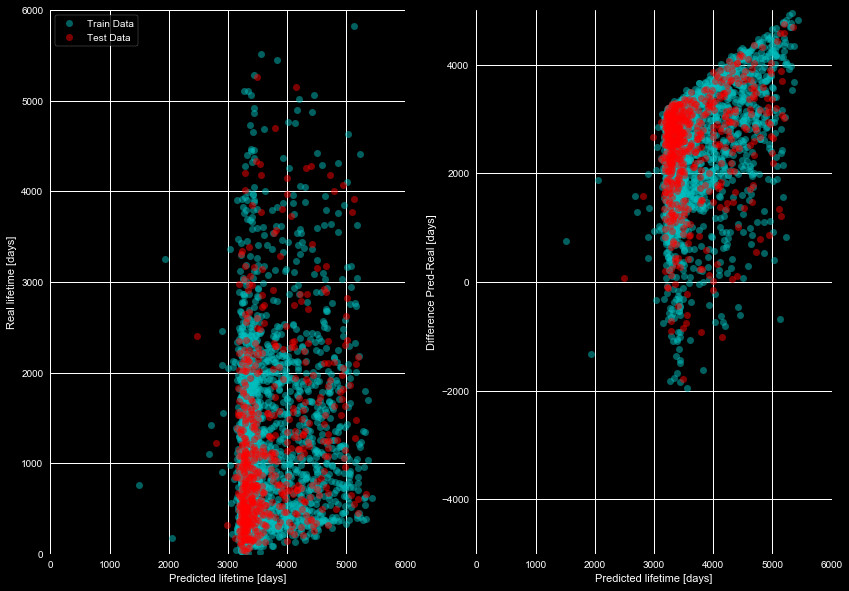

We see these policies have a long estimated lifespan. In fact, attempting

to estimate the average lifetime of just about every policy gives something

in the thousands of days, and the survival functions fail to estimate the

lifetimes. We plot our attempts at this in Figure 8, which compares the

real lifetime to that predicted from the survival functions. If there was

even a rough linear correlation we could say this model could be useful, but

it clearly fails to predict the lifetimes.

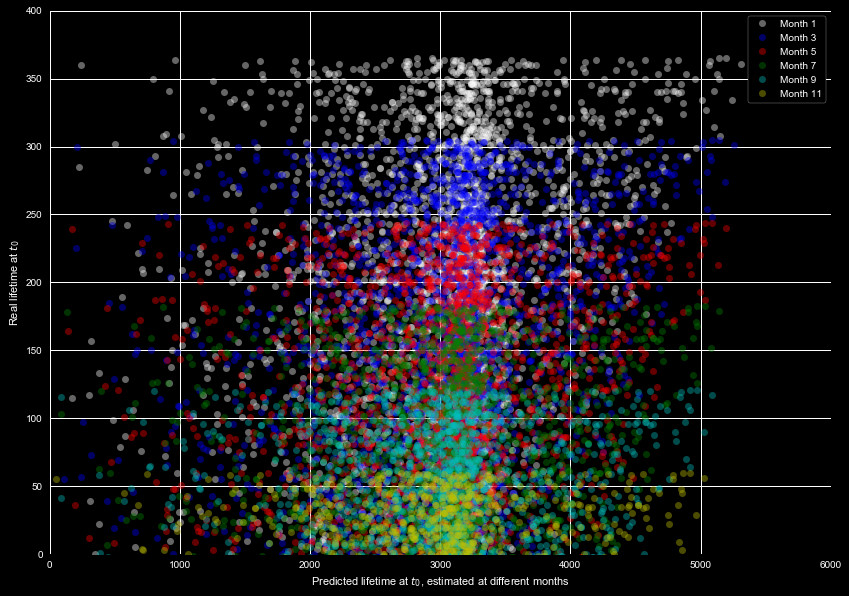

The above prediction is for the total lifetime. It's reasonable to expect

the largest uncertainty when predicting such a large value, so maybe it would

be more reasonable to estimate the remaining lifetime from the survival function.

We show this in Figure 9, which shows the real remaining lifetime, and

predicted remaining lifetime, for different months using the test data set.

A keen eye may notice the predicted values only slightly shift from month

to month. This is clearly another failed attempt to predict the lifespan.

We took this survival function, and tried predicting the likelihood of canceling

in certain months. This is found by integrating over the survival function in the

time frame of interest. This provided little help, as the survival functions predict

a less than 5% chance of cancellation for all policies, for all months. Clearly this

functions fails. The methods for analysis are simple so this does not seem to be in

the implementation.

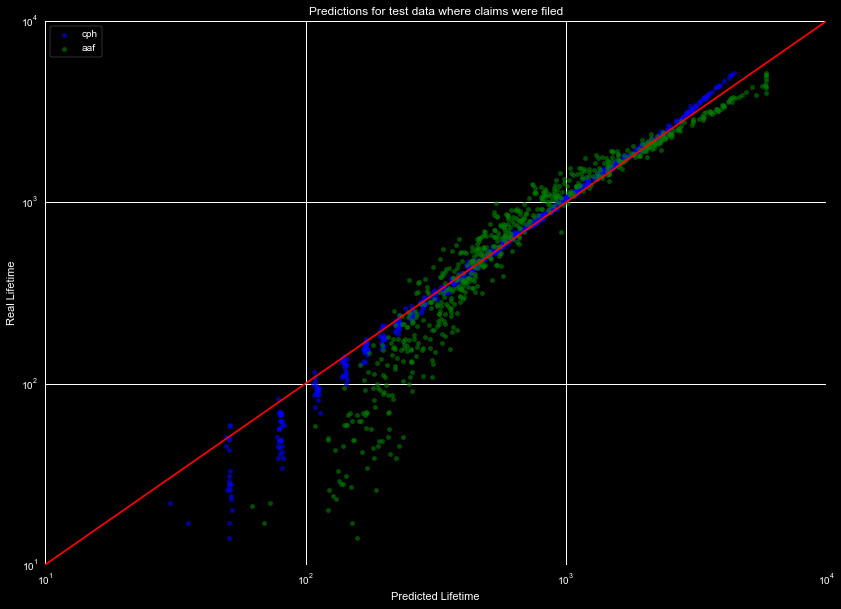

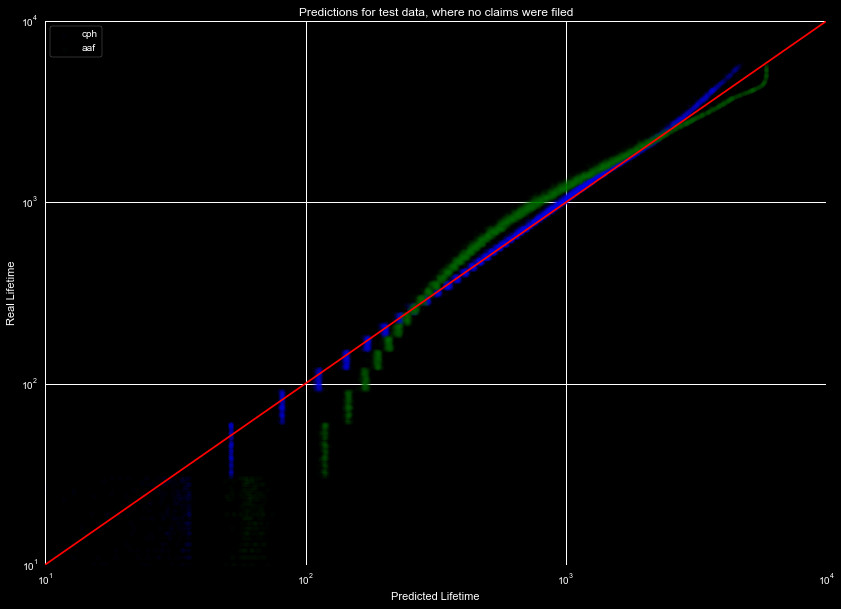

This may be due to the approach we are using. Lumping all the data into one model

may be erroneous. We have two sets of data that may demonstrate different behavior.

Roughly a third of the policies have filed claims, with the remaining have never

filed a claim. If these demonstrate different behavior, it may cause the predicted

lifetimes to be off. We thus break our data set into two different sets, those with

claims filed, and those that don't have claims filed, and plot the predicted lifespans

of the two sets in Figures 10 and 11. The models were trained on 80% of the data

in both cases, and predicted on 20% of the holdout (predicting only on data we

see the cancellation for). We see with this split,

the Aalen Additive Fitter struggles, but the Cox Proportional Hazard Fitter performs

relatively well over the whole range in both cases.

We see that splitting the data, and then modeling it, causes the predicted lifespans

to drastically improve over the group set. We will compare these models to a general

machine learning model, in our results section. First, we must generate our

Machine Learning Model.